Lesson 3 – What is GAAP?

Introduction

If your company wants to issue stock or be involved in mergers and acquisitions in the future, it is crucial to have an understanding of generally accepted accounting principles (GAAP). While accountants are responsible for GAAP, being familiar with the standards and the advantages and disadvantages of GAAP can help you hire knowledgeable financial experts and potentially impact your company’s long-term sales and stock value.

I. What Are the Generally Accepted Accounting Principles (GAAP)?

Generally accepted accounting principles (GAAP) are a set of accounting rules, standards, and procedures that are widely accepted and followed in the United States. These principles are established by the Financial Accounting Standards Board (FASB). Public companies in the U.S. are required to adhere to GAAP when preparing their financial statements.

GAAP is based on ten key principles and is a rules-based set of standards. It is often compared to the International Financial Reporting Standards (IFRS), which is considered to be more principle-based. IFRS is a global standard and there have been recent efforts to transition from GAAP to IFRS in financial reporting.

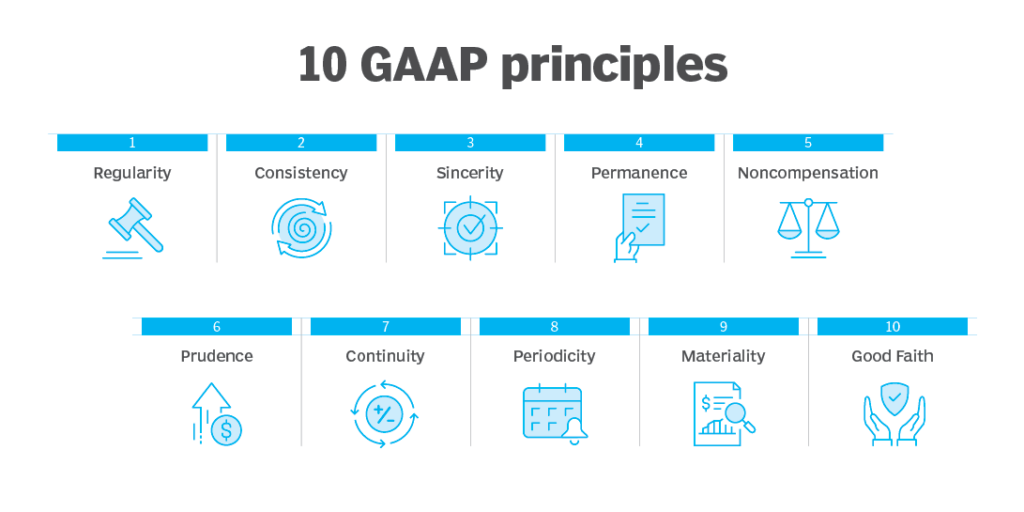

II. The 10 Key Principles of GAAP

Regularity Principle

The accountant has followed the standard rules and regulations of GAAP.

Consistency Principle

Accountants are committed to using the same standards consistently in their financial reporting, ensuring comparability between periods. Any changes or updates to the standards should be fully disclosed and explained in the footnotes of the financial statements.

Sincerity Principle

The accountant aims to provide an accurate and unbiased representation of a company's financial situation.

Permanence of Methods Principle

The procedures used in financial reporting should be consistent, allowing for a comparison of the company's financial information.

Non-Compensation Principle

Both positive and negative aspects should be reported transparently, without expecting any debt compensation.

Prudence Principle

This principle emphasizes the representation of financial data based on facts, without speculation.

Continuity Principle

When valuing assets, it is assumed that the business will continue to operate.

Periodicity Principle

Entries should be recorded in the appropriate accounting periods. For example, revenue should be reported in the relevant period.

Materiality Principle

Accountants must strive to disclose all financial data and accounting information in financial reports.

Utmost Good Faith Principle

Derived from the Latin phrase "uberrimae fidei" used in the insurance industry, this principle assumes that all parties involved remain honest in all transactions.

III. Applying GAAP in the workplace

Accountants follow GAAP by using Financial Accounting Standards (FAS) issued by the FASB. The FASB was established in 1973 and has released over 100 FAS pronouncements. Before the FASB, other organizations like the American Institute of Certified Public Accountants Accounting Standards Committee, the Accounting Principles Board (APB), and the Committee on Accounting Procedure (CAP) also played a role in setting GAAP. Some accounting standards from the APB and CAP are still in effect today.

While the FASB and its predecessors are responsible for most of GAAP, additional rules can be found in statements from the Financial Reporting Executive Committee (FinREC) of the AICPA. There are also accepted best practices that are not formal pronouncements but are widely used. For example, it is generally assumed that financial statements are based on the belief that a company will continue to operate.

IV. FAQ

Where Are Generally Accepted Accounting Principles (GAAP) Used?

GAAP is a set of procedures and guidelines that companies use to prepare their financial statements and other accounting disclosures. These standards are created by the Financial Accounting Standards Board (FASB), an independent non-profit organization. The purpose of GAAP is to ensure that the financial information provided to investors and regulators is accurate, reliable, and consistent.

Why is GAAP important?

GAAP is important because it helps maintain trust in the financial markets. Without GAAP, investors would be hesitant to trust the information presented by companies, leading to less confidence in its integrity. This lack of trust could result in fewer transactions, higher transaction costs, and a weaker economy. GAAP also allows investors to compare companies more easily, making it simpler to analyze their performance.

What are non-GAAP measures?

Companies are allowed to present certain figures that do not adhere to GAAP guidelines, as long as they identify them as such. They may do this when they believe that GAAP rules do not capture certain nuances of their operations. In these cases, they may provide specially designed non-GAAP metrics in addition to the required GAAP disclosures. However, investors should be cautious of non-GAAP measures, as they can sometimes be used misleadingly.

What is the difference between IFRS and GAAP?

In terms of conceptual approach, GAAP is more rule-based while IFRS is more principle-based. GAAP is primarily used in the United States, while IFRS is an international standard. Both standards cover various areas such as inventories, investments, long-lived assets, extraordinary items, and discontinued operations.

Conclusion

In conclusion, the GAAP is essential for creating a consistent, clear, and comparable method of accounting. It also ensures that a company’s financial records are complete and consistent. This is important for business leaders because it provides a comprehensive understanding of the company’s financial health.