Lesson 2 – External and Internal Users and Uses of Accounting

Introduction

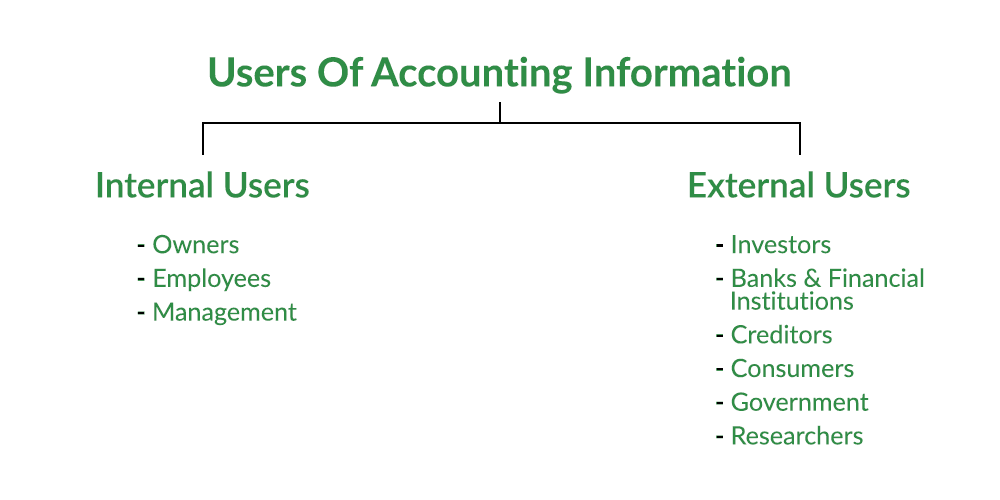

Accounting information is essential for various users to make informed decisions. These users can include business owners, employees, investors, and government entities. Users of accounting information can be divided into two categories: internal users and external users.

I. Internal Users

1. Owners

Owners are individuals who invest their money and time into growing a business. They have a keen interest in understanding the financial position of the business and whether it has made a profit or suffered a loss. Financial statements provide valuable information about the business’s financial position and its earnings or losses.

2. Managers

Managers are responsible for overseeing and controlling the business. They make important decisions and develop strategies for the business’s growth. Managers rely on financial information to make plans and policies for future actions, such as determining sale prices, managing costs, identifying problems, and implementing corrective measures.

3. Employees

Employees, who work for a company, are also interested in reviewing financial reports. They want to know about the company’s earnings and prospects to make informed decisions about their own career growth and job security. Many employees examine the accounting information provided in the annual report to gain a better understanding of the company’s operations. Some companies even offer company shares to their employees, which further increases their interest in accounting information.

II. External Users

1. Banks And Investors

Banks and Investors play a crucial role in businesses by providing loans or investments. They closely monitor the performance of the business to assess its financial position and prospects. Positive growth ensures the safety of their investment and the repayment of the loan.

2. Consumers

While not all consumers require accounting information, some industrial consumers rely on it. These consumers purchase goods in large quantities and establish long-term relationships with suppliers. They need accounting information to make informed decisions when selecting the right suppliers.

3. Creditors

Creditors are individuals or entities that provide goods or services to a business on credit. They are interested in knowing whether the company will be able to repay its debts and how much credit they can extend to the company. Financial statements play a crucial role in helping creditors make these decisions.

4. Government

The government also relies on financial statements to ensure that companies are adhering to rules and regulations. This information assists the government in making policy decisions. Tax authorities, which are government-owned entities, use financial statements to determine if a company is accurately reporting and paying its taxes.

5. Public

The general public may also seek financial information about a company. This could include journalists looking for news stories or individuals interested in joining the company as employees. Additionally, researchers utilize accounting information in their research work.

Conclusion

In summary, internal financial reporting is the process of using various tools and techniques by managers within a company to plan, budget, and monitor performance. On the other hand, external financial reporting involves the use of these tools and techniques by investors, lenders, suppliers, or other parties outside the organization.